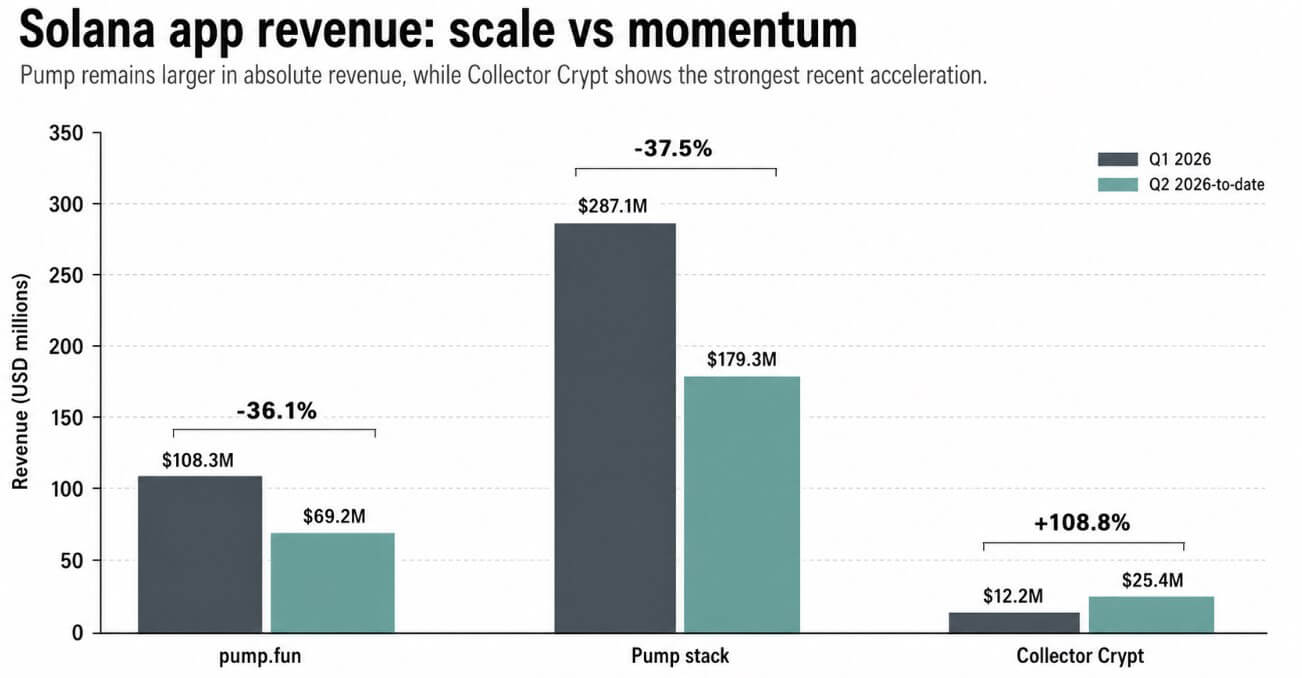

According to recent data from DefiLlama, Pump.fun garnered an impressive $108.3 million in gross revenue during Q1 and has accrued $69.2 million so far in Q2. This marks a significant decline of 36.1% from the previous quarter’s performance.

When taking into account the entire Pump suite, which includes PumpSwap and Terminal along with Pump.fun, the gross protocol revenue for Q2 to date stands at $179.3 million. This figure is a steep 37.5% lower than Q1’s $287.1 million. Earnings also saw a decline, dropping from $120.9 million to $79.1 million in the same timeframe.

Pump.fun ranks among the top contenders in profitability among consumer applications developed on the Solana blockchain. Its cumulative revenue has surpassed $1 billion, while the entire Pump suite has generated $1.18 billion since its inception.

Notably, the platform utilizes a bonding-curve mechanism which not only provides initial liquidity for new token issues but also collects fees on various trading activities. This mechanism continues to facilitate hundreds of millions in decentralized exchange (DEX) volume each month.

The quarter-on-quarter comparison highlights a slowing momentum, with cumulative revenue and volume showcasing one of the most effective consumer loops in the crypto space.

In contrast, the revenue conversation on Solana is expanding, particularly with Collector Crypt’s numbers demonstrating growth as Pump.fun experiences a downturn.

A Different Trajectory

On the other hand, Collector Crypt is a Solana protocol that centers around tokenized physical trading cards. Users engage by purchasing randomized digital packs linked to actual, graded cards, allowing them to trade these tokenized cards on-chain, resell them via the platform, or redeem the physical items.

Described by DefiLlama as a platform for trading RWA (real-world asset) Pokémon cards on Solana, Collector Crypt generates revenue through pack sales, marketplace fees, and royalties, accounted for after buybacks of gacha packs.

Recently, Collector Crypt launched over 215,000 tokenized TCG packs in just one week and exceeded $50 million in cumulative revenue, with more than 30% of users opting to redeem physical cards.

DefiLlama reports that Collector Crypt generated $12.3 million in Q1 and surged to $25.8 million in Q2 up until now, marking a striking 108.8% growth.

The platform’s 7-day revenue of $5.1 million represents about 38% of its total 30-day revenue of nearly $13.5 million, in contrast to Pump.fun’s 22.8% ratio, indicating stronger recent activity concentration.

Collector Crypt’s 30-day figures account for 88.3% of its total $123.5 million in cumulative DEX volume, while Pump.fun records a mere 1.4%, indicating a protocol whose activity is both recent and on an upward trajectory.

In terms of revenue for 2026, Collector Crypt has achieved $38.1 million, representing approximately 21.5% of Pump.fun’s $177.5 million and 8.2% of the broader Pump stack’s $466.5 million.

The data clearly illustrates that while one protocol is experiencing deceleration, another is gaining momentum.

| Metric | Pump.fun | Broader Pump Stack | Collector Crypt | Readout |

|---|---|---|---|---|

| 2026 Revenue | $177.5M | $466.5M | $38.1M | Pump remains the larger revenue generator YTD |

| Cumulative Revenue | $1.0B+ | $1.18B | $58.4M | Pump demonstrates historical scale |

| 7-day Revenue / 30-day Revenue | 22.8% | ~23.0% | 38.0% | Collector Crypt exhibits stronger recent concentration |

| 30-day DEX Volume / Cumulative Volume | 1.4% | N/A | 88.3% | Collector Crypt’s tracked activity is more recent |

| Main Revenue Loop | Token Launches | Launches, Swaps, Terminal | Tokenized Trading Card Packs | Distinct consumer behaviors |

CARDS as a Market Indicator

Collector Crypt’s token, CARDS, has closely followed the upward trend in the protocol’s revenue. CoinGecko lists CARDS at approximately $0.259, indicating a recent 47% rise within a week. The token has around $10.4 million in 24-hour trading volume and a market cap of roughly $66.83 million, with an all-time high recorded at $0.38.

CARDS serves as a liquid instrument for traders to reflect their expectations regarding the growth of Collector Crypt. However, it’s essential for token holders to understand that revenue capture should not be directly equated with these price movements.

DefiLlama currently indicates that Collector Crypt holders’ revenue is virtually zero, citing that tracking will resume once the protocol’s buyback hub wallet secures official verification.

Examining the broader landscape of tokenized trading cards, the top seven platforms amassed $230 million in gacha sales during May 2026, a figure that represents a sevenfold increase year-over-year, with Solana contributing 64% of this volume.

This growth underscores a particular aspect of Solana’s consumer application economy and its potential monetization avenues.

Pump.fun’s operational model relies on a speculative issuance loop: new tokens launch, engage in bonding curves, and eventually shift to open markets, generating fees throughout each phase. Conversely, Collector Crypt’s approach revolves around consumer engagement via randomized pack openings linked to recognizable physical collectibles, encouraging on-chain trading and tangible asset redemption.

Although both models generate fees, trading volume, and active token markets, they attract distinct user motivations and define value differently for on-chain assets.

Looking Ahead: Future Projections

If Collector Crypt maintains its current revenue momentum while the broader tokenized trading card market continues its expansion, the protocol could solidify its position in Solana’s app revenue hierarchy.

With CARDS acting as a liquid representation of this growth, the sustained demand for gacha packs will contribute to closing the revenue gap with Pump.fun further.

The recently reported sevenfold income spike across the tokenized trading card sector supports this optimistic forecast, granting user demand remains consistent.

Conversely, should the allure of gacha demand diminish, if CARDS volume declines, or if jurisdictions begin imposing scrutiny on loot-box frameworks tied to randomized pack mechanics, Collector Crypt’s current activity concentration may become a potential risk rather than proof of its resilience.

Given the cumulative revenue of $58.4 million is comparatively minor against Pump.fun’s $1 billion, any downturn in demand could quickly manifest in the weekly metrics that currently illustrate Collector Crypt’s growth trajectory.

| Scenario | Projected Outcomes | Metrics to Monitor | Market Implications |

|---|---|---|---|

| Base Case: Widespread Attention, No Replacement | Pump remains the dominant revenue generator while Collector Crypt maintains visibility in app revenue rankings | Pump’s 30-day revenue stabilizes; Collector Crypt continues elevated 7-day/30-day ratio | Solana’s consumer revenue diversifies beyond merely memecoin issuances |

| Collector Crypt Momentum Persists | Gacha demand remains high, CARDS continues as the liquid market indicator, and 30-day revenue gap narrows | Pack openings, 30-day revenue, CARDS volume, redemption activities | Tokenized collectibles potentially become a viable long-term Solana consumer category |

| Pump Experiences Reacceleration | If memecoin issuance rebounds, PumpSwap/Terminal could compensate for Pump.fun’s cooling | Pump stack’s 7-day revenue and DEX volume rebounds | The divergence may be a temporary shift in momentum |

| Collector Crypt Cooldown | Declining gacha demand, diminishing CARDS volume, or increasing scrutiny of loot boxes | Decline in 7-day/30-day ratio, lower demand for packs, reduced token activity | Recent concentration may turn into a liability, rather than a sign of sustained growth |

Collector Crypt is predicated on the notion that consumers will pay for, trade, and engage with digital assets that are tied to recognizable physical items.

The Q2 results convey that both this model and Pump.fun’s framework can generate substantial fees simultaneously on the same blockchain, indicating that Solana’s consumer revenue landscape is broader than it was at the beginning of the year.

{kind=link}