Apyx’s token, apxUSD, faced a notable depreciation on June 4, dipping below its intended dollar peg as Bitcoin hovered around $63,000. This development reignited concerns regarding the risks associated with DeFi stablecoins.

A report from Bitget indicated that apxUSD briefly reached a low of $0.93 during a selloff phase. It characterized Apyx’s response as a deliberate design feature. Specifically, the reserve risk for apxUSD is predominantly assigned to Strategy’s STRC preferred stock, with cash acting as a supplementary buffer.

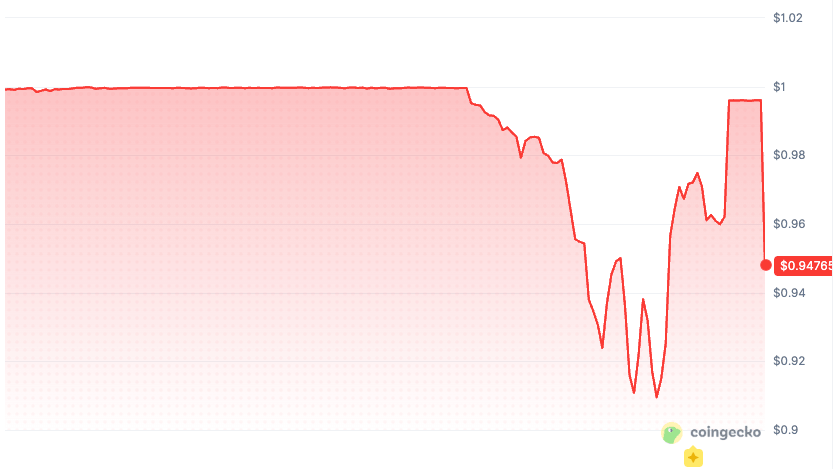

At that moment, data revealed a significant fluctuation in apxUSD’s value, with a trading range between $0.9094 and $0.9984, and the token trading at approximately $0.9176 with a volume of about $74.6 million.

In contrast to a typical stablecoin crisis, the mechanics surrounding apxUSD place it in a unique category. The cryptocurrency fell by 5.77% within a 24-hour period, reflecting a broader market trend impacting the token, alongside the public-market shares becoming part of the DeFi collateral framework.

A Dollar Token Built on Preferred Equity

Apyx positions apxUSD as a synthetic dollar, underpinned by a collection of preferred shares issued by Digital Asset Treasury companies. This structure enables apxUSD to function as collateral as well as a quoted asset across both DeFi and CeFi ecosystems, channeling the generated yield from the collateral stack back into apyUSD, which serves as the protocol’s savings asset.

The STRC preferred stock represents the core collateral for apxUSD, as outlined in Apyx’s peg stability model. STRC operates on a $100 stated value, leveraging an economic structure to maintain stability through dividend adjustments that foster trading near the reference price.

Viewing a dollar token through the lens of preferred share collateral may not align with traditional views shaped by USDC’s model. Apyx emphasizes overcollateralization, along with a cash and Treasury buffer, as well as possible cross-market arbitrage opportunities and hedging strategies. Their risk management section acknowledges that apxUSD’s trading value might exceed or fall short of the $1 benchmark.

This perspective reframes the June 4 incident as a market-structure event, raising the question of whether DeFi participants accurately assess a dollar-like asset whose collateral is akin to public preferred equity during times of market stress.

In contrast, Circle maintains a different reserve model for USDC, asserting that it is redeemable 1:1 for actual dollars and supported by a diverse portfolio of highly liquid cash and cash-equivalents. The majority of USDC reserves reside within the Circle Reserve Fund, encompassing cash, short-dated U.S. Treasuries, and overnight Treasury repurchase agreements.

Apyx’s approach to backing capital is dynamic, allowing for fluctuations across DAT preferred shares, with cash and short-term Treasuries contributing to liquidity. Kraken’s listing note specifies that minting and redemption of apxUSD are confined to authorized institutional participants, with redemptions executed in USDC, while the underlying preferred equity remains outside the flow of redemption.

Understanding the access model is crucial during volatile conditions. An authorized participant is typically granted a primary route through the protocol, while regular holders are left navigating the market dynamics, whether on a decentralized exchange (DEX), centralized exchange order book, or other DeFi avenues.

Apyx’s FAQ section also directly addresses liquidity risk, noting that users acquiring apxUSD via DEX swaps may encounter slippage during periods of low liquidity. Additionally, it mentions that apyUSD exits operate on an asynchronous model with a cooldown period of approximately 30 days.

This results in an instrument resembling a stablecoin, whose dollar parity is determined by factors beyond the issuer’s stated price. Essential considerations include the market price of STRC, the liquidity depth of the apxUSD/USDC pair, whitelisted arbitrage opportunities, the reserve buffer’s composition, and the demand for exits among DeFi users at any given time.

Preferred Shares as a Risk Factor in DeFi

The significance of STRC extends beyond the background, as its design encapsulates perpetual preferred stock obligations, paying an annual cash dividend of 11.50%, with monthly adjustments to promote trading stability around the $100 par value.

Also highlighted is the caveat that returns, liquidity, future performance, and cash dividends are not guaranteed, particularly as the preferred securities lack collateral claims on Strategy’s Bitcoin holdings.

Strategy’s recent filing added complexity to the market’s interpretation of this structure. In a June 1 Form 8-K, it was revealed that the company sold 32 BTC between late May and early June for about $2.5 million, with the proceeds anticipated to fund distributions for their preferred stock.

The filing confirmed that Strategy retained 843,706 BTC as of the end of May and held the STRC dividend rate steady at 11.50% for the upcoming monthly periods starting June 1.

This background has set the stage for a market intricately linking Strategy’s preferred dividends, Bitcoin treasury liquidity, the par-seeking design of STRC, and DeFi collateral products.

As previously noted by CryptoSlate, the preferred stack has played a crucial role in Strategy’s financing mechanism, shedding light on the risks tied to selling BTC to sustain preferred payouts, thus making STRC an essential indicator of funding conditions.

Now, apxUSD brings this complexity into the DeFi sphere. The preferred share has transitioned from being merely a capital-markets instrument accessible via brokerage accounts to an on-chain dollar product employed as liquidity, collateral, and yield-generating infrastructure.

The selloff experienced on June 4 revealed this interlinking. DAT preferred shares are marketed as low-volatility, income-generating instruments associated with crypto-holding companies, transforming public-market yields into programmable stablecoin infrastructure.

While DeFi can harness attractive yields, it must also contend with interconnected risks related to credit, liquidity, confidence, and exit routes.

The upcoming challenge is clear: Should STRC trend back toward par, and apxUSD’s liquidity stabilize, leading to a recovery in the token’s value toward its expected reference point, this scenario may present a real-world stress test for a design that Apyx has acknowledged as allowing for price variability.

Conversely, if STRC maintains a discount, the reserve metrics indicate inadequate cushioning, or if DeFi platforms report liquidations or emergency parameter modifications, the market might begin to redefine apxUSD’s role as less of a typical stablecoin and more as a credit-linked collateral asset.

Key signals for the market will include: STRC’s pricing relative to par, the current reserve structures of Apyx, depths of liquidity for apxUSD/USDC transactions, exposure levels within Pendle and Curve, Morpho’s collateral behavior, and any adjustments to Strategy’s dividend rates.

Bringing Wall Street’s preferred equity into the DeFi arena essentially bestows it with a market price, which subsequently becomes a significant component of the collateral risk equation.

{kind=link}